Spring Sales Surge as the Coachella Valley Market Hits Its Seasonal Stride

The Hamilton Real Estate Group April 13, 2026

The Hamilton Real Estate Group April 13, 2026

The Coachella Valley real estate market closed out March with a strong seasonal push, as sales volume reached its highest point in three years and buyer demand accelerated through the end of the valley's peak season. With 733 homes sold — an 11% gain over March 2025 and a 39% jump from February — the market sent a clear signal that buyer conviction is solid heading into spring. Inventory continued to pull back from year-ago levels, tightening market conditions and keeping the valley on solid footing even as some price metrics reflect broader buyer caution.

March delivered 733 closed sales across the Coachella Valley, a 39% surge from February's 527 and 11% ahead of the 660 sales recorded in March 2025. That year-over-year gain is particularly meaningful: it marks the strongest March sales performance in at least three years. The volume increase reflects both the seasonal pull of the valley's prime buying window and growing buyer engagement as the spring market gains momentum.

Active listings fell to 3,514 in March — down 7% from February and nearly 14% below the 4,081 homes available in March 2025. The Month's Supply of Inventory (MSI) dropped sharply to 4.79, down 33% from the prior month and 22% below March 2025. An MSI under 5 is approaching seller's market territory, and this reading suggests the supply-demand balance is tightening in a meaningful way. Buyers have fewer choices than they did a year ago, and that dynamic is worth watching.

The median sale price in March held steady at $619,000, unchanged from February and modestly below March 2025's $627,000 — a 1% decline year-over-year. The average sale price came in at $917,036, off 3% from February and 2% below March 2025. The two metrics are telling a similar story: prices are not declining sharply, but year-over-year comparisons show modest softening from the elevated levels of early 2025. Given the strong sales volume, this pricing environment reflects a healthy and realistic market rather than a distressed one.

Price per square foot came in at $388 in March — flat from February and down 4% from $403 in March 2025. As the most normalized measure of property value, this metric removes the distortion of home size and product mix, offering a cleaner read on where values stand. The year-over-year dip is modest and consistent with the measured price recalibration visible across other metrics. No meaningful acceleration in either direction is underway.

Homes averaged 88 days on market in March, up slightly from 85 days in February and 17% higher than the 75-day average in March 2025. The year-over-year increase is the most significant signal here: buyers across the valley are taking more time before committing, and that pace has been building steadily over the past year. For sellers, this reinforces the importance of competitive pricing from the outset — homes that sit tend to lose negotiating leverage as time passes.

The sale-to-list price ratio held at 97% in March, unchanged from both February and March 2025. That consistency — flat for three consecutive comparison periods — points to a market where expectations on both sides are reasonably well-calibrated. Sellers who price realistically are achieving near-asking results; those who push above market value are the ones absorbing discounts.

March brought 1,154 new listings to market, up 7% from February's 1,083 but 15% below the 1,351 new listings in March 2025. The month-over-month uptick reflects normal seasonal patterns as more sellers enter the market in spring. However, the year-over-year decline means the pipeline of fresh inventory remains constrained relative to a year ago.

The March data paints a more competitive picture for buyers than the prior few months. Inventory is down sharply from a year ago and sales are running ahead of last year's pace — meaning there is more competition for a smaller pool of available homes. Days on market remain elevated compared to 2025, which does offer some breathing room on well-priced properties, but buyers should not mistake longer market times as a sign of seller weakness across the board. Homes are still selling for 97% of list price, so strong offers on well-positioned properties remain necessary.

For sellers, March's data is genuinely encouraging. Sales volume is at a three-year high while inventory is tightening. That said, the 97% sale-to-list ratio and modest year-over-year price softening are reminders that the market rewards realistic pricing, not optimism. Sellers who come to market well-priced and well-prepared are achieving near-asking results. Those who price ahead of current value risk sitting as days on market continue to trend above prior-year levels.

Mortgage rates have shown modest improvement in recent weeks, with the 30-year fixed currently averaging approximately 6.4%, the 15-year fixed at around 5.7%, and the 30-year jumbo at approximately 6.5% — all meaningfully below the peak levels seen in 2023. Both the 30-year and 15-year fixed rates have edged down from the prior week, a welcome development for buyers actively shopping the market.

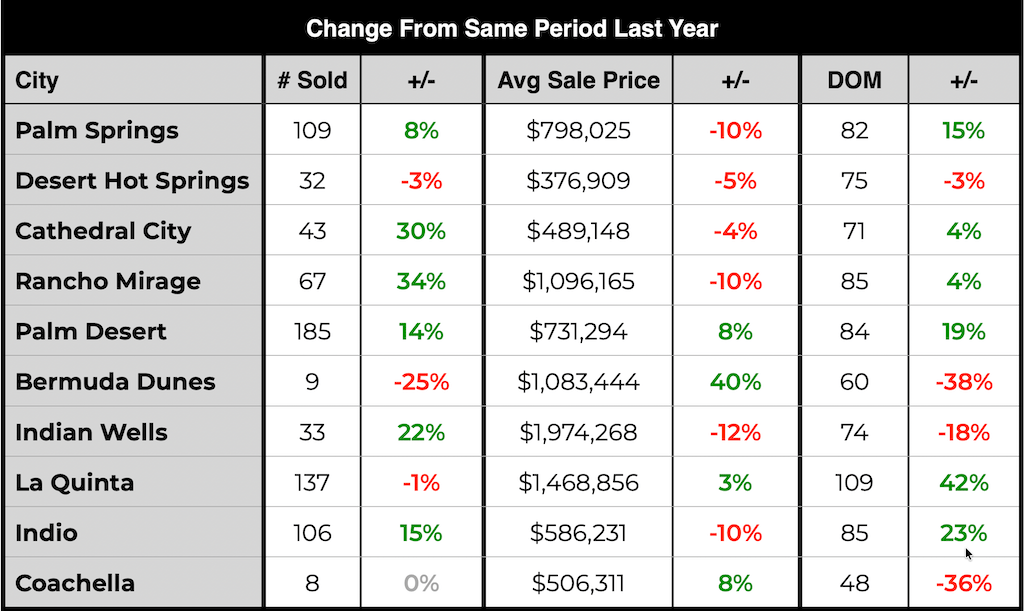

March's sales picture was broadly positive across the valley, with several cities posting standout year-over-year gains. Rancho Mirage led all markets with a 34% increase in homes sold, followed closely by Cathedral City at 30% and Palm Desert at 14%. Palm Springs added 8% more sales than a year ago, and Indio rose 15%. Indian Wells climbed 22%, notable given the higher price points in that market. The softer side of the ledger included Desert Hot Springs, down 3%, and La Quinta, essentially flat at -1%. Bermuda Dunes posted a 25% volume decline, though that market's smaller transaction count amplifies percentage swings.

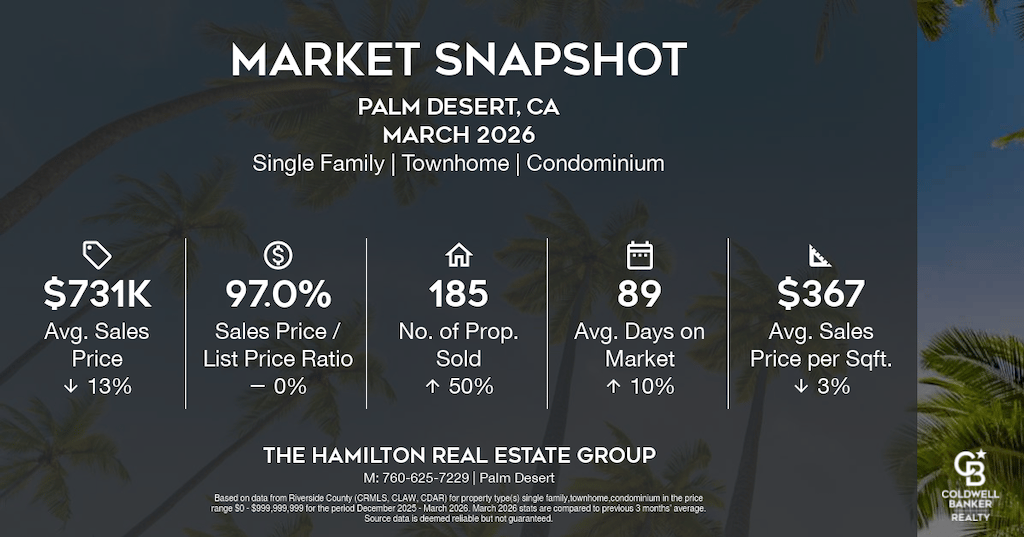

Pricing trends varied sharply by city, with Bermuda Dunes reporting a strong year-over-year gain — average prices up 40% to $1,083,444. That swing reflects a meaningful shift in the mix of homes sold there rather than across-the-board appreciation. Palm Desert was a notable bright spot, posting 8% average price growth year-over-year to $731,294, as did La Quinta with a modest 3% gain to $1,468,856 and Coachella at +8% to $506,311. On the other side, Rancho Mirage and Palm Springs each softened 10% year-over-year, while Indian Wells declined 12% to $1,974,268.

The DOM picture was mixed, with several cities showing notably longer selling timelines than a year ago. La Quinta saw the sharpest increase, with homes averaging 109 days — up 42% year-over-year — followed by Indio at 85 days, up 23%, and Palm Desert at 84 days, up 19%. Palm Springs averaged 82 days, also up 15%. Coachella and Bermuda Dunes were the bright spots, with homes selling in 48 and 60 days respectively — both well below the valley average and down meaningfully from a year ago. Indian Wells improved 18% year-over-year to 74 days, and Cathedral City held relatively steady at 71 days.

If you're considering putting your home on the market, let us help you get it SOLD! Now, more than ever, marketing matters! Our world-class marketing plan, with online ads, paid YouTube ads, and social media exposure, is critical in this shifting market. Call now for a free seller consultation, and let us help you decide if now is the right time to sell your home.

If you'd like a detailed market report for a specific city, email us and let us know which city reports you'd like to receive.

Call us at (760) 409-8811, or visit www.thehamiltonregroup.com for an easy-to-use home search and information on how we can help you with all your essential real estate needs.

The Hamilton Real Estate Group is evolving to meet all our customers' real estate needs. If you are ready to sell, call or email us, or for a FREE instant home valuation report, click here: What's My Home Worth?

Copyright © 2026 Hamilton Desert Homes, LLC. All rights reserved.

Stay up to date on the latest Coachella Valley news!

Coachella Valley home sales climbed 11% year-over-year in June as inventory tightened and prices leveled off, but homes are sitting longer

July the Coachella Valley: six July 4th events valley-wide, free concerts, dive-in movies, comedy, art shows & Dancing with the Stars Con

Valley home values held near two-year highs in May as inventory fell 17% from last year and new listings hit their lowest level since 2024.

Art festivals, Bob Dylan, ShortFest, Juneteenth, comedy icons, and outdoor movies — June in the desert is anything but quiet.

April sales climbed nearly 8% year-over-year as inventory tightened and prices moderated — a Coachella Valley market finding its footing.

Firebirds playoffs, film noir, Joshua Tree music, and Marilyn Monroe's 100th birthday — May in Greater Palm Springs doesn't slow down.

March sales hit a 3-year high as 733 Coachella Valley homes sold — up 11% year-over-year — while inventory tightened and the market gained momentum.

Coachella, Stagecoach, Desert Rodeo, Broadway, playoff hockey, and more — April in the Coachella Valley has a lot going on. Here's your guide.

The Coachella Valley real estate market gained momentum in February, with sales surging 30% and pricing holding steady as spring season approaches.

Dan and Reuben of The Hamilton Real Estate Group are here to guide you through a transformative real estate experience. Join us, and let the connection open doors to your next real estate adventure.